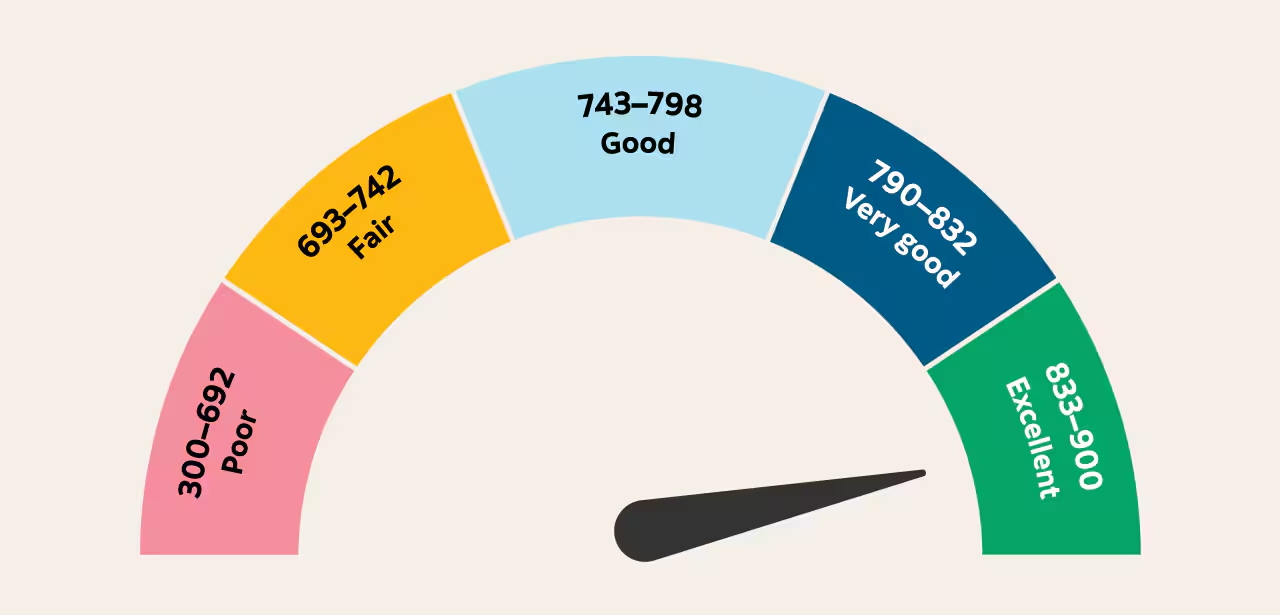

1. Credit Score—Not Just a Number

Credit scores might sound mysterious, but they’re really just a number based on your past borrowing. Like a financial report card, but without the weird gym teacher energy. Back in 1956, FICO (Fair Isaac Corporation) created the original model. Today, most U.S. lenders still rely on that system, scoring folks between 300 and 850.

The U.S. average in 2024 sat at 716, but not everyone’s hitting that mark. In fact, over 42 million Americans have no score at all, either because they never borrowed or their file’s too thin.

Think of your credit score like a financial selfie. It’s not the full picture of who you are, but banks, landlords, and even some employers peek at it to decide if they want to deal with you. In most countries, this three-digit number ranges from 300 to 850. The higher it is, the easier life gets when you’re borrowing money, signing a lease, or even buying a phone on installments.

Back in 2023, the average FICO score in the U.S. was 718, while in 2010, it was around 687. That 31-point jump didn’t happen overnight. It took better financial literacy, mobile apps like Credit Karma, and fewer post-2008 financial disasters.

What most folks don’t realize? Your score doesn’t care if you’re rich. You could earn $200K a year and still have a score of 520 if you miss bills or max out your cards. Meanwhile, someone making $40K could sit pretty at 790 just by playing the game right.

2. What Makes Up Your Score?

Five ingredients go into cooking your credit score:

- Payment History (35%) – Paying bills on time is king. Missed a payment in 2022? That red mark could haunt you until 2029.

- Amounts Owed (30%) – This is your credit utilization. Use more than 30% of your limit and the score frowns.

- Length of Credit History (15%) – Old accounts = good news. That dusty 2007 student card still matters.

- Credit Mix (10%) – Variety helps: a mortgage, a car loan, a credit card? Sweet balance.

- New Credit (10%) – Opening too many new lines at once? Your score says, “Whoa, slow down.”

In 2015, the average American had about 3 credit cards, and in 2024, that number crept up to 3.8. More plastic doesn’t automatically help—managing it wisely does.

Each piece plays its part. Ignore any one, and your score might take a nosedive. For example, someone with $8,000 of debt on a $10,000 limit is using 80%—a huge red flag to lenders.

3. Why Your Score Matters (More Than You Think)

Lenders see your score like a risk radar. A score above 750 means you’ll likely get the best deals: lower interest rates, higher loan approvals, and smoother approvals on rentals. In 2023, someone with a 780 credit score got a 30-year mortgage at 5.9%, while a person with 620 paid around 7.4%. That 1.5% difference? It added up to over $52,000 across the loan’s lifetime.

Insurance companies also peek at your score. Drivers with low credit pay 29% more on average for car insurance. Meanwhile, landlords are more likely to rent to someone with a 700+ score, especially in competitive markets like New York or L.A.

Even some jobs check credit. Around 16% of employers used credit reports in hiring as of 2020. Want a job in finance or government? That score might be your silent reference.

A low score doesn’t just make life expensive—it makes it complicated. You might need a co-signer for apartments, pay higher deposits for utilities, or get denied for travel credit cards offering cool perks like lounge access or cashback.

4. How to Boost Your Score Without Magic

No spells, just smart moves. First, pay everything on time. In 2022, over 35% of score dips came from just one late payment. Set reminders or auto-pay to dodge forgetfulness.

Second, keep your credit utilization low. If you’ve got a $5,000 card, try keeping the balance under $1,500. Requesting a limit increase (without spending more) can help. In 2021, users who kept utilization under 10% had an average score of 781.

Third, don’t close old accounts. That 2009 credit card you never use? It adds to your “length of history.” Cancel it, and your score might shrink. Also, check your reports. In 2023, over 42 million Americans found errors in their credit reports. Fixing those mistakes bumped scores by up to 45 points on average.

Lastly, don’t apply for credit every month. Each application dings your score a little. Space them out, and if you’re denied, figure out why before trying again. In 2025, even some rental apps began soft-pulling credit before approving leases.

5. Quick Fixes and Myths to Avoid

Some people think paying off collections deletes them instantly—it doesn’t. They stick around for up to 7 years, even if paid. But newer scoring models like FICO 9 and 10 ignore paid collections, so lenders using those might go easier on you.

Another myth? Checking your score hurts it. Nope—only “hard” checks from lenders impact scores. Your own peeks are “soft” and harmless. In 2022, over 68% of millennials avoided checking their score due to this myth. That’s like not weighing yourself because you’re afraid to see the number.

Also, beware of credit repair scams. If someone guarantees a 100-point boost overnight for a fee? Run. In 2020, the FTC cracked down on over 20 companies promising fake results.

Want a fast bump? Ask a family member with great credit to add you as an “authorized user.” If they’ve had a card since 2010 and always paid on time, their good behavior can help you—without you ever touching their card.

6. Tools, Apps, and Habits That Help

Technology’s on your side. Apps like Credit Sesame, Experian Boost, and Mint make tracking easy. In 2023, Experian Boost helped users increase their score by an average of 13 points just by linking utility and streaming payments.

Budgeting consistently matters too. Those who used apps like YNAB (You Need A Budget) in 2022 reported 90% fewer late payments compared to those budgeting with spreadsheets. Automate what you can—savings, bills, alerts.

Make credit a monthly ritual. Spend 20 minutes reviewing your accounts. In 2019, a study showed that users who checked their reports quarterly improved scores 23% faster than those who didn’t.

Avoid buy-now-pay-later traps unless you can track them easily. In 2024, missed BNPL payments hit 12%, dragging scores unexpectedly. Treat every financial decision like it’s visible on a billboard—because to credit bureaus, it kinda is.

Final Word:

A great credit score isn’t about income—it’s about habits. Master those, and the doors open wide. Whether you’re applying for a new card, buying a car, or eyeing your dream house, that three-digit number could be your secret weapon. Start today, track it monthly, and watch your financial world get a whole lot smoother.

Want help decoding your financial life? Platforms like https://gpt-eurax-x9.jp/ offer tools that make this journey smoother, smarter, and a whole lot less stressful.